In recent months, we have found ourselves in a scenario of much turmoil and uncertainty regarding the report of non-financial information vs CSRD. There are many unanswered questions and few clear answers guaranteeing how Spanish companies should report on sustainability. Currently, what we do know for sure is that our companies must continue reporting in accordance with the Law 11/2018 on Non-Financial Information, what we know as EINF. Want to know what the situation is? We'll tell you everything 📚✨

Index

CSRD START

We must understand that all this commotion and the need to CSRD This is indicated by the market itself, as it lacks a frame of reference. Europe, in its commitment to a decarbonized economy by 2050, continues to work on its strategy to make this decarbonization as painless as possible for businesses. To this end, the aim is to introduce an intermediate target achievable by 2040, with the publication this year of an amendment to the climate change law.

For this reason, the presentation of this first one took place at the end of January. Omnibus package, Establishing a Commission work program that focuses on a series of regulations (Corporate Responsibility, Due Diligence Directive, Taxonomy and the Carbon Border Adjustment Mechanism) that currently place an excessive burden on companies. What was the result of all this? A change in the working methodology to achieve the same objective more efficiently, adjusting the regulatory burden for companies.

CURRENT STATUS: CSRD AND BUS

Today, we must take the Omnibus Package We should approach this with caution, as we don't know how this package will be implemented in companies or how all these issues will ultimately be transposed into Spanish law. For now, it's just a proposal, which will undergo modifications until it's approved and then incorporated into our legislation. Therefore, what this is giving us... Omnibus package These are just a few hints of where they want to go, but we'll see how it all turns out in the end.

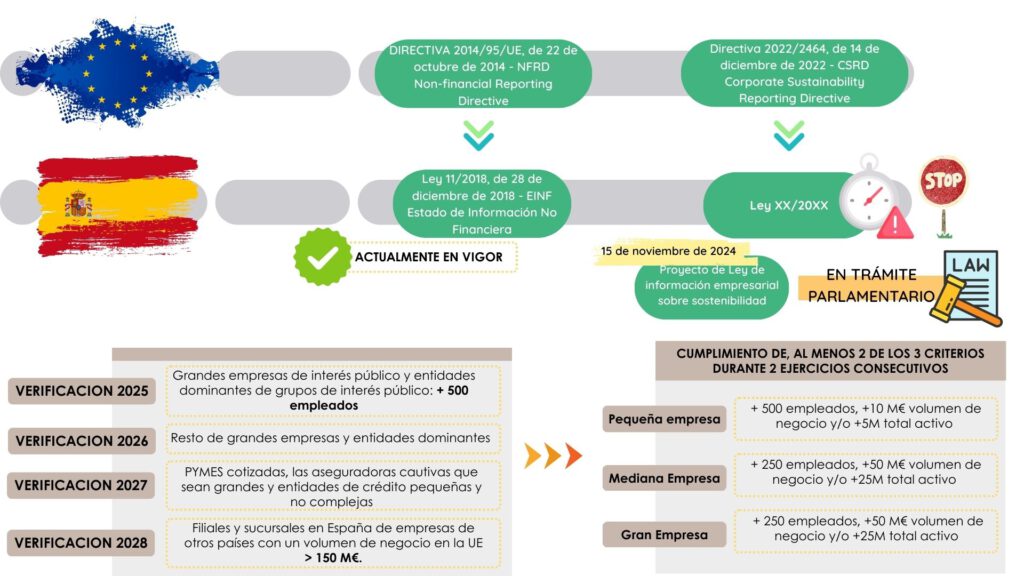

Of all the comparable aspects between CSRD and the Omnibus package, What we are clear about are the compliance deadlines. The staggered “3 waves” of compliance with the requirements for the years 2024, 2025 and 2026 are eliminated. CSRD And directly, companies are given more time to comply with all the requirements, with a 2-year deferral.⏳

With this clock stop The "stop the clock" initiative aims to ensure that the application requirements apply to certain companies (currently, we don't know what type of companies these are, but it is stipulated that they are companies with more than 1,000 employees) so that the first report, according to the relevant directive, is made in 2027. This does not represent a step backward, but rather a continuation of the process, only with simplifications, postponements, and delays, thus offering companies the necessary time to adapt to regulatory changes without incurring additional costs or facing legal uncertainties.

CSRD IN SPAIN: CALM DOWN!

But… let's not get carried away! In our country, we still don't have the transposition of the Directive 2022/2464 And of this, we only have one bill that is still in parliamentary process, so given this legal vacuum, all Spanish companies that are currently reporting in accordance with Law 11/2018, They have to keep doing it until it is definitively transposed CSRD in our country.

Summary of the current situation in Spain:

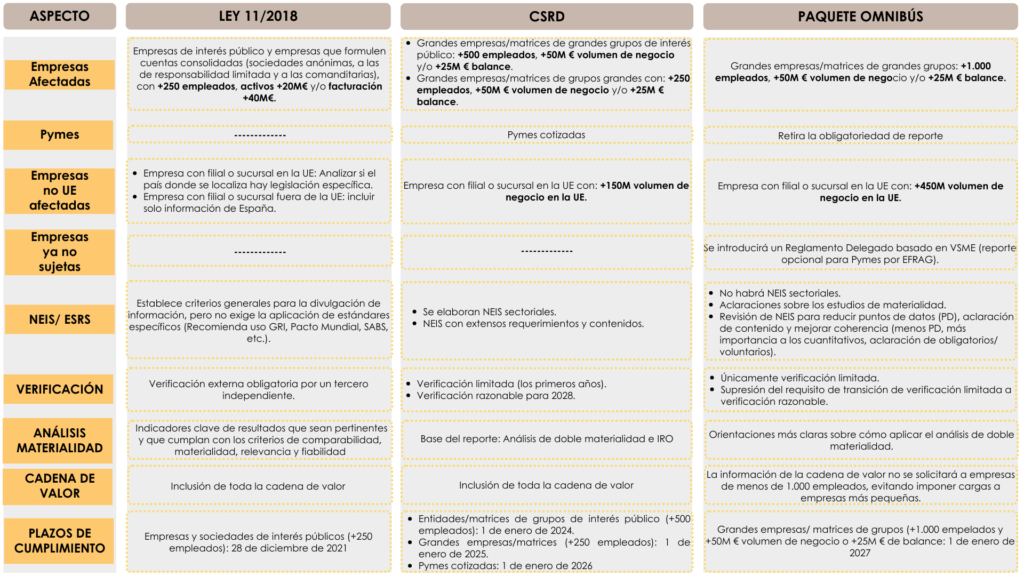

LAW 11/2018 vs CSRD vs OMNIBUS: SIMILARITIES AND DIFFERENCES

After all this commotion, what we can do is prepare ourselves for the new reporting model, clearly understanding the similarities and differences between them all.

📈 Conclusion: There's no need to panic, but we do need to prepare. Sustainability remains at the forefront, and it's crucial to be informed and ready for the transition. 🚀

#INCYMA #ConsultingSustainability #Sustainability #CSRD #PackageOmnibus #Law112018 #EINF